Page 111 - BKT Annual Report 2024 EN

P. 111

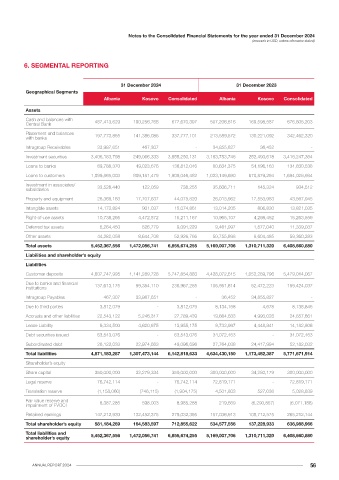

Notes to the Consolidated Financial Statements for the year ended 31 December 2024 Notes to the Consolidated Financial Statements for the year ended 31 December 2024

(amounts in USD, unless otherwise stated) (amounts in USD, unless otherwise stated)

The average effective yields of significant categories of financial assets and liabilities of the Bank as at 31 December 2023 were as follows: The interest re-pricing dates of significant categories of financial assets and liabilities of the Bank as of 31 December 2023 were as

ALL USD EUR follows:

Assets Up to 1 month 1-3 months 3-12 months 1-5 years Over 5 year Total

Cash and balances with Central Bank 3.25% - - Assets

Placement and balances with banks 3.70% 5.28% 3.86% Cash and balances with 676,805,203 - - - - 676,805,203

Central Bank

Treasury bills 4.12% - -

Placement and balances with 253,190,785 52,069,783 37,201,752 - - 342,462,320

Investment securities 3.88% 5.62% 3.84% banks

Investment securities 330,849,762 350,742,343 512,793,026 1,765,398,272 456,463,961 3,416,247,364

Loans to banks - 8.55% 7.10%

Loans to banks - - 134,830,538 - - 134,830,538

Loans to customers 6.47% 8.98% 5.34%

Loans to customers 479,688,228 74,399,146 580,511,199 249,657,693 309,772,718 1,694,028,984

Total 1,740,533,978 477,211,272 1,265,336,515 2,015,055,965 766,236,679 6,264,374,409

Liabilities

Customer deposits 1.26% 0.93% 0.85% Liabilities

Due to banks and financial institutions 3.28% 7.76% 4.07% Customer deposits 3,037,197,834 284,653,010 1,224,118,500 879,319,670 53,725,053 5,479,014,067

Due to banks and financial

Lease Labilities 6.93% 4.27% 2.32% 148,970,134 - 10,453,903 - - 159,424,037

institutions

Debt securities issued - - 4.00% Debt securities issued - - 101,912 33,970,551 - 34,072,463

Subordinated debt - - 8.51% Subordinated debt - - 52,182,032 - - 52,182,032

Total 3,186,167,968 284,653,010 1,286,856,347 913,290,221 53,725,053 5,724,692,599

The interest re-pricing dates of significant categories of financial assets and liabilities of the Bank as of 31 December 2024 are as follows: Interest rate sensitivity

The sensitivity analysis below has been determined based on the exposure to interest rates at the reporting date and the stipulated

Up to 1 month 1-3 months 3-12 months 1-5 years Over 5 year Total change taking place at the beginning of the financial year and held constant throughout the reporting period. The following is a stipulation

of effects of changes in interest rate to the net profit, when the change is applied to the GAP position as per re-pricing terms presented

Assets

in note above, assuming all the other variables are held constant:

Cash and balances with 677,670,397 - - - - 677,670,397

Central Bank 31 December 2024 31 December 2023

Placement and balances with 299,808,659 1,142,520 36,825,922 - - 337,777,101 Up to 1 year Over 1 year Up to 1 year Over 1 year

banks

Interest rate increases by 2% 9,211,697 55,157,489 14,330,923 50,616,470

Investment securities 245,519,293 329,340,412 602,943,847 1,799,314,935 678,131,644 3,655,250,131 Interest rate increases by 1.5% 6,908,773 41,368,117 10,748,192 37,962,353

Interest rate increases by 1% 4,605,849 27,578,745 7,165,461 25,308,235

Loans to banks - - 124,127,226 14,684,820 - 138,812,046

Interest rate decreases by 1% (4,605,849) (27,578,745) (7,165,461) (25,308,235)

Loans to customers 483,812,918 79,106,244 612,121,912 344,876,762 389,128,646 1,909,046,482 Interest rate decreases by 1.5% (6,908,773) (41,368,117) (10,748,192) (37,962,353)

Interest rate decreases by 2% (9,211,697) (55,157,489) (14,330,923) (50,616,470)

Total 1,706,811,267 409,589,176 1,376,018,907 2,158,876,517 1,067,260,290 6,718,556,157

(e) Operational risks

Operational risk is the risk of direct or indirect loss arising from a wide variety of causes associated with the Bank’s processes, personnel,

Liabilities technology and infrastructure, and from external factors other than credit, market and liquidity risks such as those arising from legal

and regulatory requirements and generally accepted standards of corporate behaviour. Operational risks arise from all of the Bank’s

Customer deposits 3,249,362,611 312,366,297 1,320,319,255 816,320,293 49,286,427 5,747,654,883

operations.

Due to banks and financial 206,502,949 3,052,738 27,396,964 14,634 - 236,967,285 The Bank’s objective is to manage operational risk so as to balance the avoidance of financial losses and damage to the Bank’s

institutions

reputation with overall cost effectiveness and to avoid control procedures that restrict initiative and creativity.

Debt securities issued - - 317,233 63,225,843 - 63,543,076 The implementation of controls to address operational risk is supported by the development of overall standards for the management

of operational risk in the following areas:

Subordinated debt - - 49,096,696 - - 49,096,696

• requirements for appropriate segregation of duties, including the independent authorisation of transactions

Total 3,455,865,560 315,419,035 1,397,130,148 879,560,770 49,286,427 6,097,261,940 • requirements for the reconciliation and monitoring of transactions

• compliance with regulatory and other legal requirements

ANNUAL REPORT 2024 54